Earnings Beat: Penumbra, Inc. Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

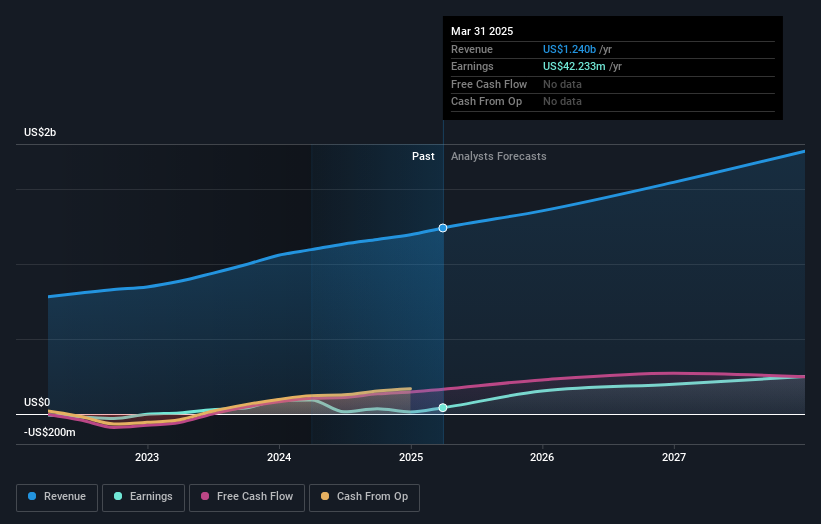

Penumbra, Inc. (NYSE:PEN) investors will be delighted, with the company turning in some strong numbers with its latest results. The company beat forecasts, with revenue of US$324m, some 2.7% above estimates, and statutory earnings per share (EPS) coming in at US$1.00, 50% ahead of expectations. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

After the latest results, the 20 analysts covering Penumbra are now predicting revenues of US$1.35b in 2025. If met, this would reflect a meaningful 9.2% improvement in revenue compared to the last 12 months. Per-share earnings are expected to surge 263% to US$3.96. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.35b and earnings per share (EPS) of US$3.63 in 2025. The analysts seems to have become more bullish on the business, judging by their new earnings per share estimates.

View our latest analysis for Penumbra

There's been no major changes to the consensus price target of US$319, suggesting that the improved earnings per share outlook is not enough to have a long-term positive impact on the stock's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Penumbra, with the most bullish analyst valuing it at US$340 and the most bearish at US$260 per share. Still, with such a tight range of estimates, it suggeststhe analysts have a pretty good idea of what they think the company is worth.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Penumbra's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 12% growth on an annualised basis. This is compared to a historical growth rate of 18% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 8.0% annually. Even after the forecast slowdown in growth, it seems obvious that Penumbra is also expected to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Penumbra's earnings potential next year. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Penumbra going out to 2027, and you can see them free on our platform here..

Before you take the next step you should know about the 2 warning signs for Penumbra that we have uncovered.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English