A Look Ahead: PagerDuty's Earnings Forecast

PagerDuty (NYSE:PD) is gearing up to announce its quarterly earnings on Thursday, 2025-03-13. Here's a quick overview of what investors should know before the release.

Analysts are estimating that PagerDuty will report an earnings per share (EPS) of $0.16.

Anticipation surrounds PagerDuty's announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

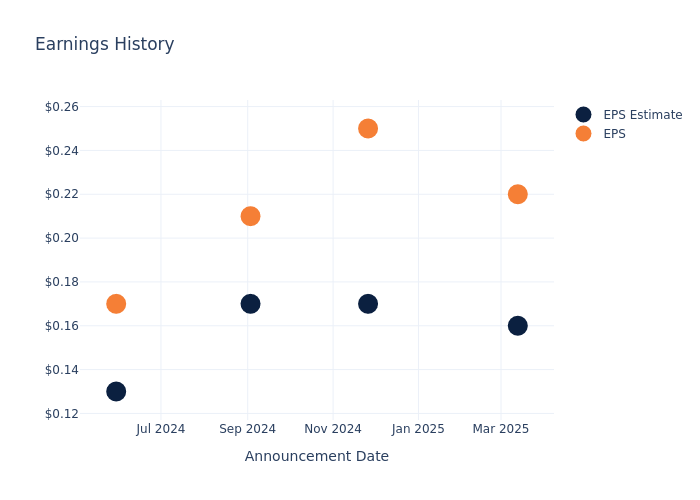

Historical Earnings Performance

In the previous earnings release, the company beat EPS by $0.08, leading to a 0.48% increase in the share price the following trading session.

Here's a look at PagerDuty's past performance and the resulting price change:

| Quarter | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 |

|---|---|---|---|---|

| EPS Estimate | 0.16 | 0.17 | 0.17 | 0.13 |

| EPS Actual | 0.22 | 0.25 | 0.21 | 0.17 |

| Price Change % | 18.0% | 0.0% | -1.0% | 6.0% |

Stock Performance

Shares of PagerDuty were trading at $14.45 as of April 21. Over the last 52-week period, shares are down 28.2%. Given that these returns are generally negative, long-term shareholders are likely upset going into this earnings release.

Analysts' Perspectives on PagerDuty

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on PagerDuty.

A total of 6 analyst ratings have been received for PagerDuty, with the consensus rating being Buy. The average one-year price target stands at $20.67, suggesting a potential 43.04% upside.

Analyzing Ratings Among Peers

The following analysis focuses on the analyst ratings and average 1-year price targets of SEMrush Hldgs and Jamf Holding, three prominent industry players, providing insights into their relative performance expectations and market positioning.

- Analysts currently favor an Buy trajectory for SEMrush Hldgs, with an average 1-year price target of $15.33, suggesting a potential 6.09% upside.

- Analysts currently favor an Neutral trajectory for Jamf Holding, with an average 1-year price target of $18.6, suggesting a potential 28.72% upside.

Peers Comparative Analysis Summary

The peer analysis summary outlines pivotal metrics for SEMrush Hldgs and Jamf Holding, demonstrating their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| PagerDuty | Buy | 9.30% | $101.47M | -8.78% |

| SEMrush Hldgs | Buy | 23.08% | $83.83M | 1.32% |

| Jamf Holding | Neutral | 8.18% | $127.77M | -2.29% |

Key Takeaway:

PagerDuty ranks at the bottom for Revenue Growth among its peers. It also has the lowest Gross Profit margin. However, it has the highest Consensus rating. Return on Equity is negative for PagerDuty, indicating lower profitability compared to its peers.

Get to Know PagerDuty Better

PagerDuty Inc is a digital operations management platform that manages urgent and mission-critical work for a modern, digital business. Its PagerDuty Operations Cloud combines artificial intelligence (AI) operations (AIOps), automation, customer service operations, and incident management with a generative AI assistant to create a flexible, resilient, and scalable platform to protect revenue and improve customer experience, improve operational efficiency, and mitigate the risk of operational failures. The company generates revenue predominantly from cloud-hosted software subscription fees and term-license software subscription fees. Geographically, the firm derives a majority of its revenue from the United States and the rest from International markets.

A Deep Dive into PagerDuty's Financials

Market Capitalization Analysis: Below industry benchmarks, the company's market capitalization reflects a smaller scale relative to peers. This could be attributed to factors such as growth expectations or operational capacity.

Revenue Growth: PagerDuty's remarkable performance in 3 months is evident. As of 31 January, 2025, the company achieved an impressive revenue growth rate of 9.3%. This signifies a substantial increase in the company's top-line earnings. As compared to its peers, the revenue growth lags behind its industry peers. The company achieved a growth rate lower than the average among peers in Information Technology sector.

Net Margin: The company's net margin is a standout performer, exceeding industry averages. With an impressive net margin of -8.73%, the company showcases strong profitability and effective cost control.

Return on Equity (ROE): PagerDuty's financial strength is reflected in its exceptional ROE, which exceeds industry averages. With a remarkable ROE of -8.78%, the company showcases efficient use of equity capital and strong financial health.

Return on Assets (ROA): PagerDuty's ROA excels beyond industry benchmarks, reaching -1.18%. This signifies efficient management of assets and strong financial health.

Debt Management: PagerDuty's debt-to-equity ratio is notably higher than the industry average. With a ratio of 3.57, the company relies more heavily on borrowed funds, indicating a higher level of financial risk.

To track all earnings releases for PagerDuty visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English