China Health Technology Group Holding (HKG:1069) Has Debt But No Earnings; Should You Worry?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that China Health Technology Group Holding Company Limited (HKG:1069) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is China Health Technology Group Holding's Debt?

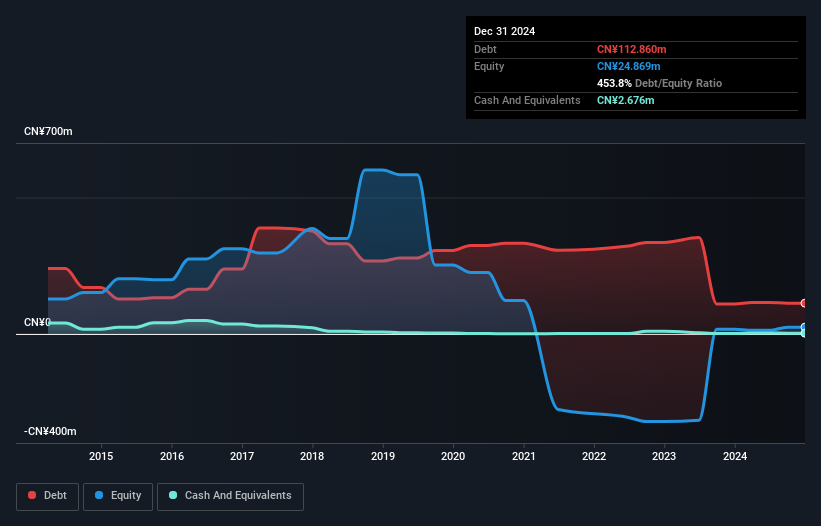

As you can see below, China Health Technology Group Holding had CN¥112.9m of debt, at December 2024, which is about the same as the year before. You can click the chart for greater detail. However, it does have CN¥2.68m in cash offsetting this, leading to net debt of about CN¥110.2m.

How Strong Is China Health Technology Group Holding's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that China Health Technology Group Holding had liabilities of CN¥53.4m due within 12 months and liabilities of CN¥112.9m due beyond that. On the other hand, it had cash of CN¥2.68m and CN¥23.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥139.9m.

The deficiency here weighs heavily on the CN¥33.7m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, China Health Technology Group Holding would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since China Health Technology Group Holding will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

See our latest analysis for China Health Technology Group Holding

In the last year China Health Technology Group Holding wasn't profitable at an EBIT level, but managed to grow its revenue by 9.1%, to CN¥60m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, China Health Technology Group Holding had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping CN¥22m. Combining this information with the significant liabilities we already touched on makes us very hesitant about this stock, to say the least. That said, it is possible that the company will turn its fortunes around. But on the bright side the company actually produced a statutory profit of CN¥3.6m and free cash flow of CN¥2.4m. So there is arguably potential that the company is going to turn things around. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for China Health Technology Group Holding you should be aware of, and 1 of them is potentially serious.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

② More than 40M Downloads Globally : data based on Webull Technologies Limited's internal statistics as of July 14, 2023.

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English