Is Sprocomm Intelligence (HKG:1401) Using Too Much Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Sprocomm Intelligence Limited (HKG:1401) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Sprocomm Intelligence

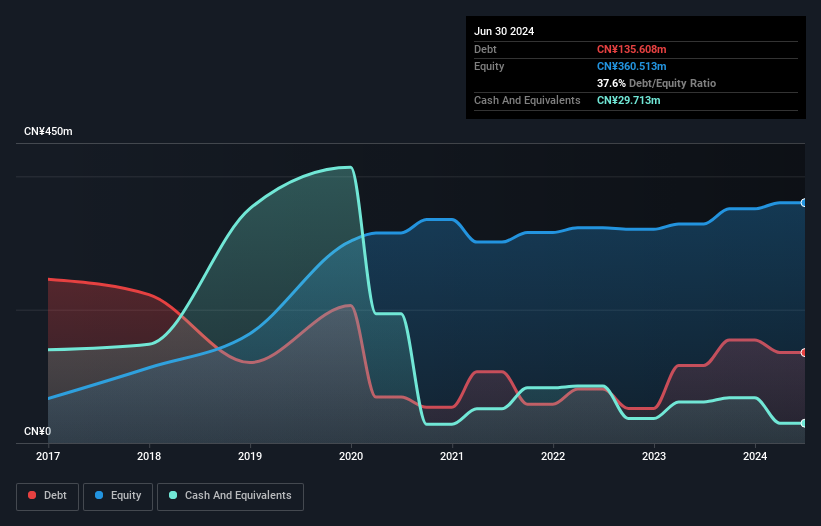

How Much Debt Does Sprocomm Intelligence Carry?

You can click the graphic below for the historical numbers, but it shows that as of June 2024 Sprocomm Intelligence had CN¥135.6m of debt, an increase on CN¥116.4m, over one year. On the flip side, it has CN¥29.7m in cash leading to net debt of about CN¥105.9m.

A Look At Sprocomm Intelligence's Liabilities

Zooming in on the latest balance sheet data, we can see that Sprocomm Intelligence had liabilities of CN¥2.52b due within 12 months and liabilities of CN¥63.7m due beyond that. On the other hand, it had cash of CN¥29.7m and CN¥585.9m worth of receivables due within a year. So it has liabilities totalling CN¥1.96b more than its cash and near-term receivables, combined.

Since publicly traded Sprocomm Intelligence shares are worth a total of CN¥13.4b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Carrying virtually no net debt, Sprocomm Intelligence has a very light debt load indeed.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Even though Sprocomm Intelligence's debt is only 2.1, its interest cover is really very low at 1.8. This does have us wondering if the company pays high interest because it is considered risky. In any case, it's safe to say the company has meaningful debt. Notably, Sprocomm Intelligence made a loss at the EBIT level, last year, but improved that to positive EBIT of CN¥38m in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But it is Sprocomm Intelligence's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Sprocomm Intelligence actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

When it comes to the balance sheet, the standout positive for Sprocomm Intelligence was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. In particular, interest cover gives us cold feet. When we consider all the elements mentioned above, it seems to us that Sprocomm Intelligence is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 3 warning signs for Sprocomm Intelligence (1 is a bit concerning!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

② More than 40M Downloads Globally : data based on Webull Technologies Limited's internal statistics as of July 14, 2023.

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English