3 SEHK Stocks Estimated To Be Up To 45.6% Below Intrinsic Value

As global markets navigate a complex economic landscape, the Hong Kong market has experienced fluctuations, with the Hang Seng Index recently declining by 2.11%, reflecting broader challenges such as deflationary pressures and economic growth concerns. In this environment, identifying undervalued stocks can present opportunities for investors seeking to capitalize on discrepancies between market prices and intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Plover Bay Technologies (SEHK:1523) | HK$5.10 | HK$10.13 | 49.6% |

| BYD Electronic (International) (SEHK:285) | HK$33.40 | HK$63.48 | 47.4% |

| Giant Biogene Holding (SEHK:2367) | HK$52.35 | HK$98.18 | 46.7% |

| Kuaishou Technology (SEHK:1024) | HK$46.65 | HK$88.47 | 47.3% |

| MicroPort NeuroScientific (SEHK:2172) | HK$9.71 | HK$18.81 | 48.4% |

| Yadea Group Holdings (SEHK:1585) | HK$12.52 | HK$23.20 | 46% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.50 | HK$55.63 | 48.8% |

| Hangzhou SF Intra-city Industrial (SEHK:9699) | HK$10.24 | HK$19.52 | 47.5% |

| DPC Dash (SEHK:1405) | HK$66.40 | HK$130.72 | 49.2% |

| Akeso (SEHK:9926) | HK$66.00 | HK$123.28 | 46.5% |

Underneath we present a selection of stocks filtered out by our screen.

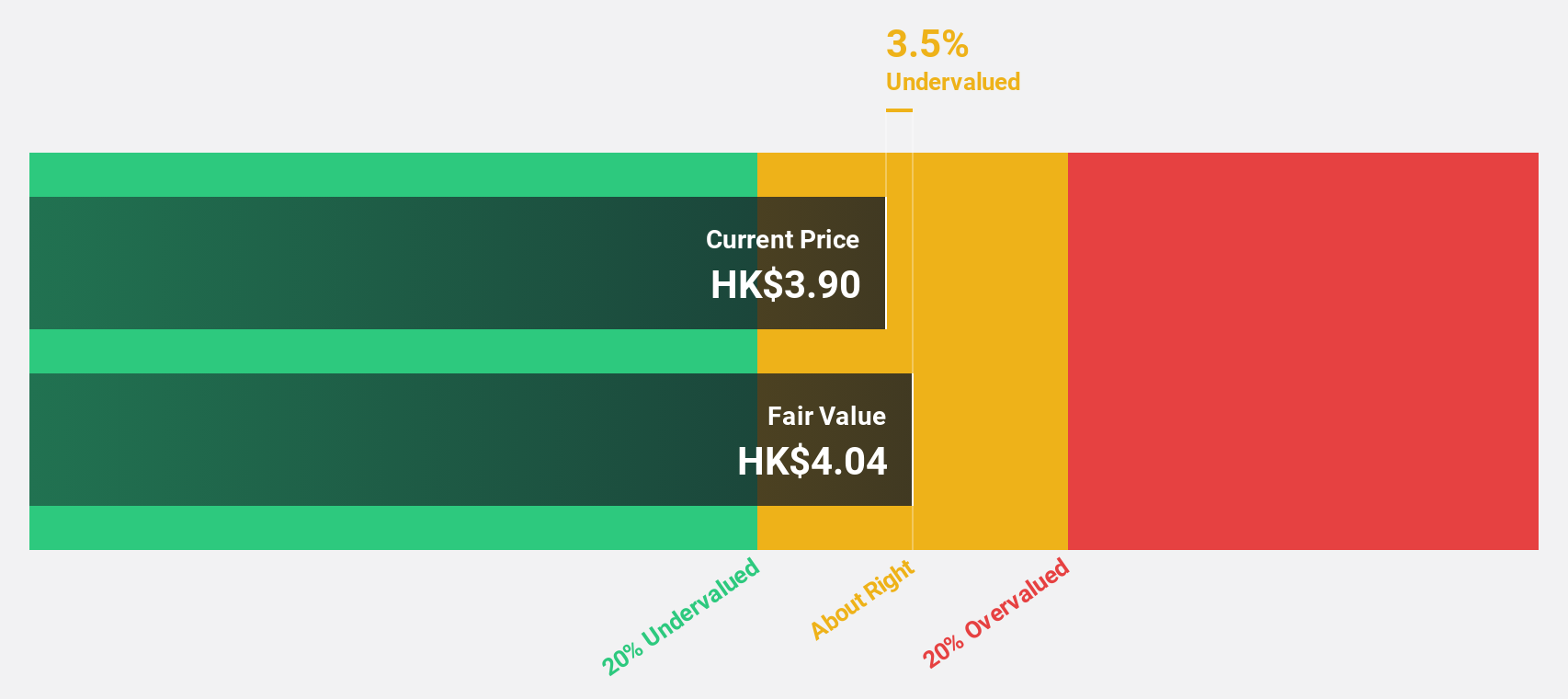

United Company RUSAL International (SEHK:486)

Overview: United Company RUSAL International is involved in the production and trading of aluminium and related products in Russia, with a market cap of HK$39.43 billion.

Operations: The company generates revenue primarily from its Aluminium segment at $10.48 billion and Aluminous products at $4.49 billion.

Estimated Discount To Fair Value: 38.9%

United Company RUSAL International is trading at HK$2.59, significantly below its estimated fair value of HK$4.24, suggesting undervaluation based on cash flows. The company's earnings are forecast to grow over 100% annually, outpacing the Hong Kong market average growth rate. However, concerns arise as debt is not well covered by operating cash flow and recent financial results include large one-off items. A potential share buyback program worth up to 15 billion could influence stock valuation positively.

- Our expertly prepared growth report on United Company RUSAL International implies its future financial outlook may be stronger than recent results.

- Take a closer look at United Company RUSAL International's balance sheet health here in our report.

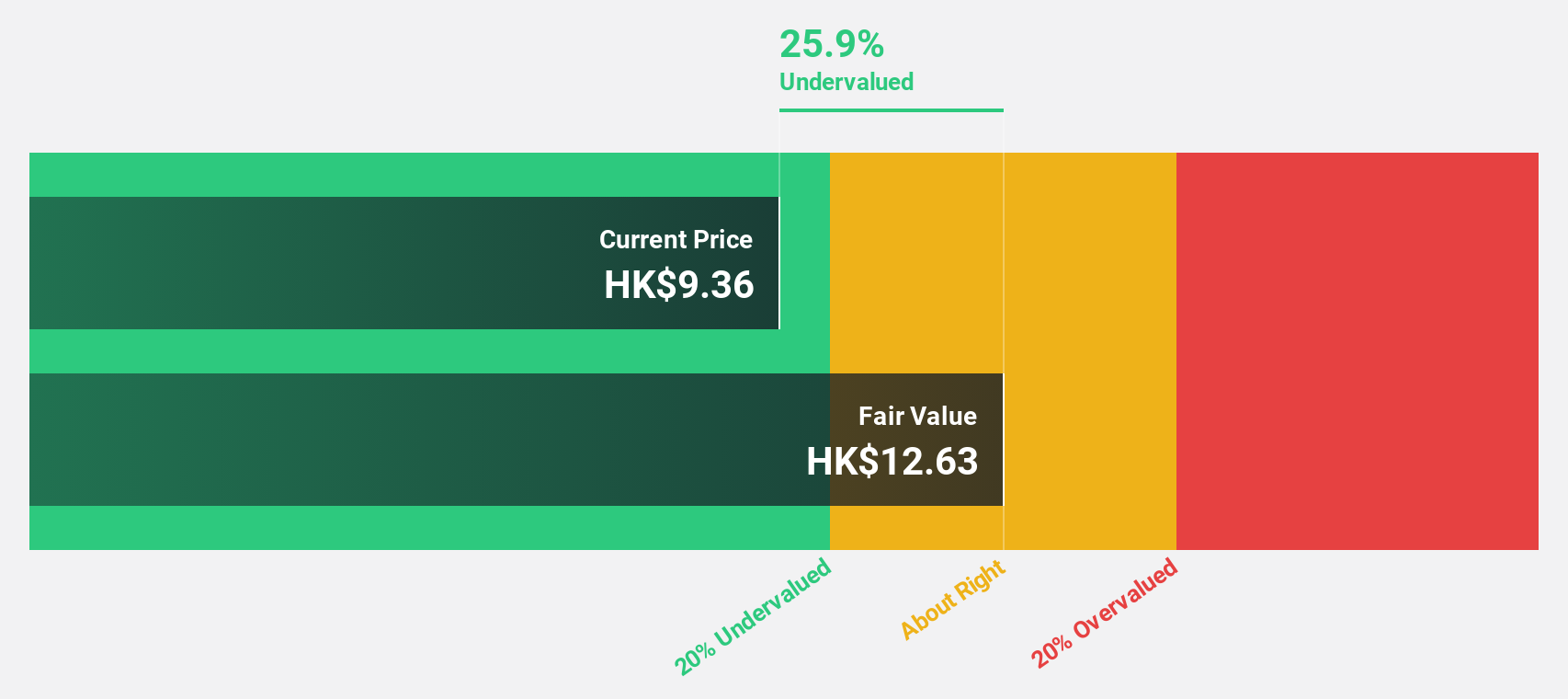

CSC Financial (SEHK:6066)

Overview: CSC Financial Co., Ltd. is an investment banking firm offering services in Mainland China and internationally, with a market capitalization of HK$197.78 billion.

Operations: The company's revenue is primarily derived from Wealth Management (CN¥7.56 billion), Transaction and Institutional Customer Service (CN¥6.84 billion), Investment Banking (CN¥3.41 billion), and Asset Management Business (CN¥1.37 billion).

Estimated Discount To Fair Value: 45.6%

CSC Financial is trading at HK$9.36, significantly below its estimated fair value of HK$17.19, highlighting undervaluation based on cash flows. Earnings are projected to grow over 30% annually, surpassing the Hong Kong market average growth rate of 12.1%. Despite these positives, recent financial results show a decline in revenue and net income compared to last year. The resignation of a key board member may also impact future strategic direction and risk management oversight.

- Insights from our recent growth report point to a promising forecast for CSC Financial's business outlook.

- Delve into the full analysis health report here for a deeper understanding of CSC Financial.

ZJLD Group (SEHK:6979)

Overview: ZJLD Group Inc is involved in the production and sale of baijiu products in China, with a market cap of HK$25.86 billion.

Operations: The company's revenue is primarily derived from its baijiu product lines, with Zhen Jiu contributing CN¥4.98 billion, Li Du generating CN¥1.29 billion, Xiang Jiao accounting for CN¥844.13 million, and Kai Kou Xiao bringing in CN¥388.16 million.

Estimated Discount To Fair Value: 15.6%

ZJLD Group is trading at HK$7.63, below its estimated fair value of HK$9.04, suggesting it may be undervalued based on cash flows. Despite a decline in profit margins from 33.1% to 19.5%, earnings are expected to grow significantly by over 20% annually, surpassing the Hong Kong market average of 12.1%. Recent earnings show increased sales but decreased net income compared to last year, with potential shareholder dilution concerns impacting valuation perspectives.

- Our earnings growth report unveils the potential for significant increases in ZJLD Group's future results.

- Dive into the specifics of ZJLD Group here with our thorough financial health report.

Next Steps

- Navigate through the entire inventory of 38 Undervalued SEHK Stocks Based On Cash Flows here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

② More than 40M Downloads Globally : data based on Webull Technologies Limited's internal statistics as of July 14, 2023.

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English