Tian Lun Gas Holdings Full Year 2023 Earnings: Misses Expectations

Tian Lun Gas Holdings (HKG:1600) Full Year 2023 Results

Key Financial Results

- Revenue: CN¥7.73b (up 2.4% from FY 2022).

- Net income: CN¥479.6m (up 7.9% from FY 2022).

- Profit margin: 6.2% (up from 5.9% in FY 2022). The increase in margin was driven by higher revenue.

- EPS: CN¥0.49 (up from CN¥0.45 in FY 2022).

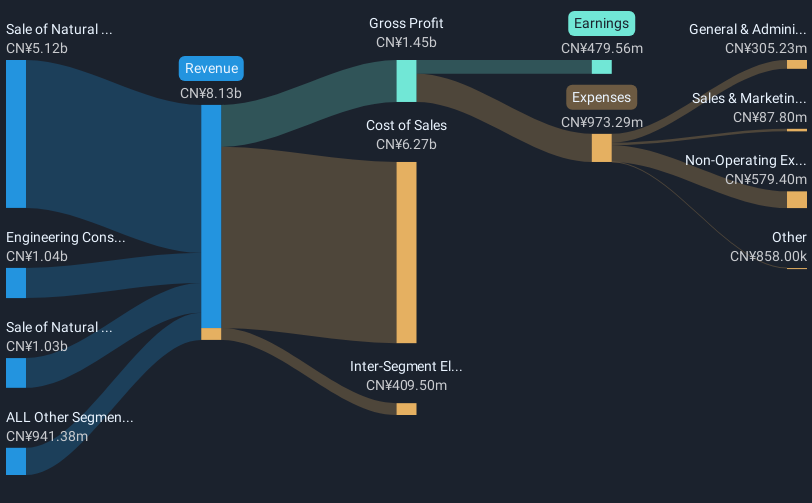

All figures shown in the chart above are for the trailing 12 month (TTM) period

Tian Lun Gas Holdings Revenues and Earnings Miss Expectations

Revenue missed analyst estimates by 3.3%. Earnings per share (EPS) also missed analyst estimates by 21%.

The primary driver behind last 12 months revenue was the Sale of Natural Gas in Cylinders segment contributing a total revenue of CN¥5.12b (66% of total revenue). Notably, cost of sales worth CN¥6.27b amounted to 81% of total revenue thereby underscoring the impact on earnings. The most substantial expense, totaling CN¥579.4m were related to Non-Operating costs. This indicates that a significant portion of the company's costs is related to non-core activities. Explore how 1600's revenue and expenses shape its earnings.

Looking ahead, revenue is forecast to grow 3.7% p.a. on average during the next 3 years, compared to a 5.5% growth forecast for the Gas Utilities industry in Hong Kong.

Performance of the Hong Kong Gas Utilities industry.

The company's shares are up 3.2% from a week ago.

Risk Analysis

We don't want to rain on the parade too much, but we did also find 2 warning signs for Tian Lun Gas Holdings (1 makes us a bit uncomfortable!) that you need to be mindful of.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

① During the campaign period, US stocks, US stocks short selling, US stock options, Hong Kong stocks, and A-shares trading will maintain at $0 commission, and no subscription/redemption fees for mutual fund transactions. $0 fee offer has a time limit, until further notice. For more information, please visit: https://www.webull.hk/pricing

② More than 40M Downloads Globally : data based on Webull Technologies Limited's internal statistics as of July 14, 2023.

Webull Securities Limited is licensed with the Securities and Futures Commission of Hong Kong (CE No. BNG700) for carrying out Type 1 License for Dealing in Securities, Type 2 License for Dealing in Futures Contracts and Type 4 License for Advising on Securities.

English